By Patrick Bateman

This post was written on August 31, 2020.

Greed = Low Interest Rates

The low interest environment and policy of quantitative easing is easily the most misunderstood, misappropriated, gossiped and ignored issue impacting our lives in the 21st Century. An issue of contradictions. Depending on who you speak to it is the source of all our ills or it is saving us. It is the conspiracy theory of gold nuts, it is the bible of Keynesian ideologues. It is trickling benefits into the economy, it is creating massive inequality. It is debated regularly in the financially-literate bubbles of society, it is never discussed among the mainstream press or among the public. The problem is that the numbers do not lie. Central bank policy is the main source of greed in the 21st Century.

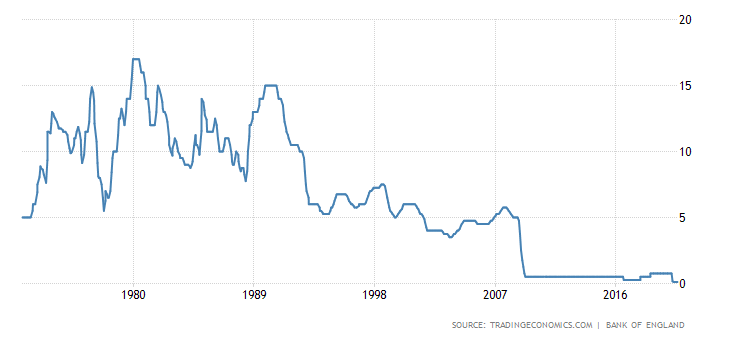

We can go back to the late 1990s when the dangerous addiction and reliance by the financial system with lower interest rates and central bank intervention started. We know these beginnings as the “Greenspan put”.

In the 1990s, the market came to believe that the US Federal Reserve, then chaired by Alan Greenspan, was effectively providing the same sort of service for the market as a whole by guaranteeing that it would underwrite it at a certain level. Hence the phrase ‘Greenspan put’. This belief was vindicated by the Fed’s prompt action in cutting rates in tricky moments, such as in the wake of the LTCM hedge-fund crisis, and by its willingness to keep rates low throughout the 1990s.

https://moneyweek.com/glossary/greenspan-put

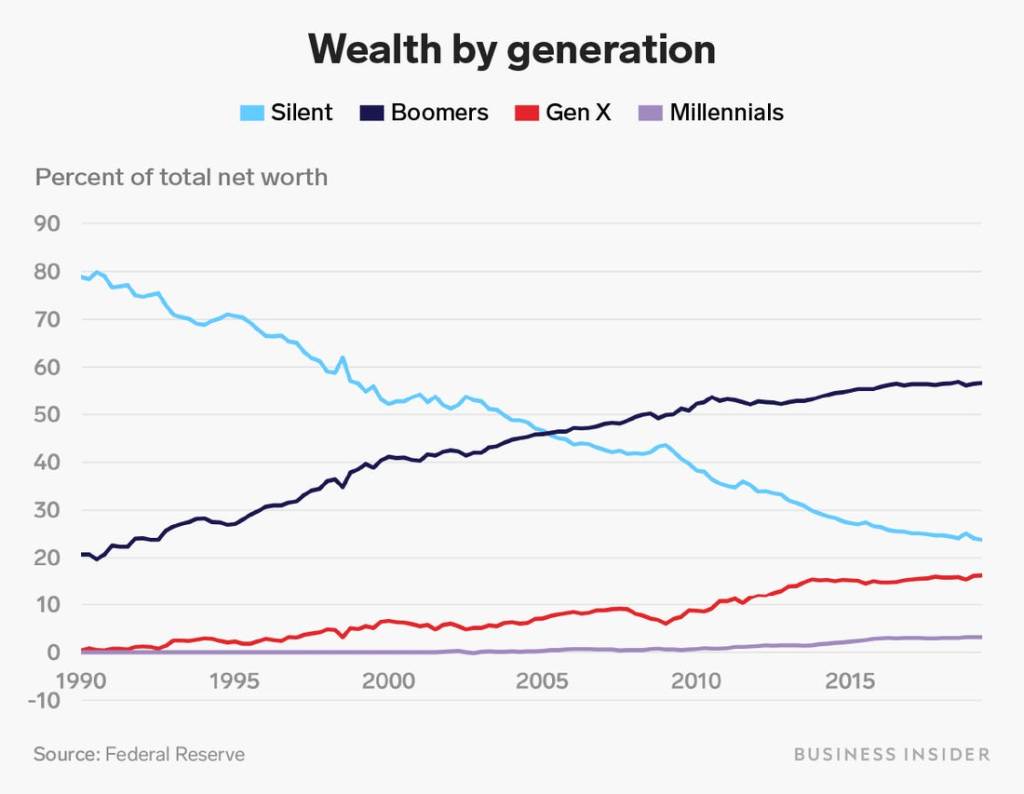

The dramatic decline of interest rates since the 1980s has been remarkable. This led to a massive accumulation of wealth by the “Baby Boomer” generation. Our elders of today are more wealthy than any other generation before. What will happen to all of this prosperity? We often hear about the great wealth transfer that is about to take place.

According to a wealth transfer report by the Royal Bank of Canada, when this group passes on their assets to younger family members, analysts expect them to leave $4tn of wealth to millennials within the UK and North America alone. This ‘inheritance boom’ will position millennials who have baby boomers in their families to receive record sums of inheritance.

https://www.bbc.com/worklife/article/20181205-with-boomers-wealth-to-inherit-will-millennials-get-rich

Forecasts rarely ever become reality and reality is not linear. Economists and bankers can project the massive wealth transfer to the younger generations until they are blue in the face, this will most likely not be on the scale currently imagined.

Asset prices have been inflated by interest rates. The longer prices go up the more risks to the downside there are and ultimately boomer wealth will collapse. Might it be possible that this wealth transfer will take place only when our parents no longer need to consume this wealth, so they hand it over to their kids just as (or before) the bubble pops? Over the long run, greed does not provide for a happy ending. Yet it is not the greediest that suffer the most.

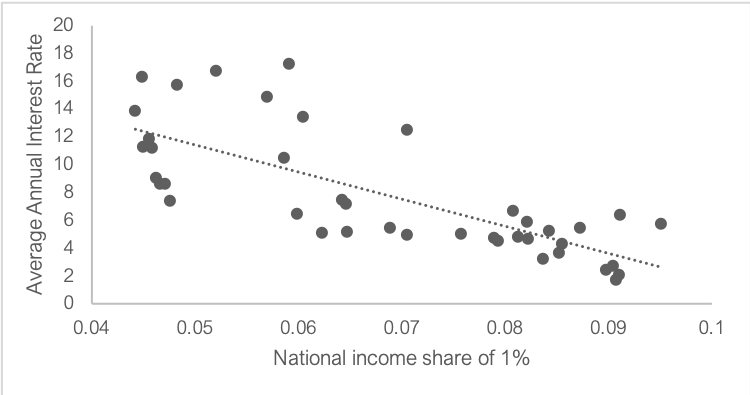

The massive spike in asset values has escalated massive wealth disparity. This inequality, spawned by persistently low interest rates, is not just a generational issue. There is no doubting the correlation among low interest rates and rising inequality. Yes there are other factors, but few have been so consistent over our present century.

The above chart focuses on Australia, but you can see the same theme across all major developed economies. Low interest rates have contributed to increased wealth concentration for the haves over the have nots. What does one need to have? Assets. Stocks. Housing. Bonds. If you have any of these and enough wealth to scale acquisition of them you are doing well. Since 2008 the rate of income differentials between the haves and the have nots has only increased.

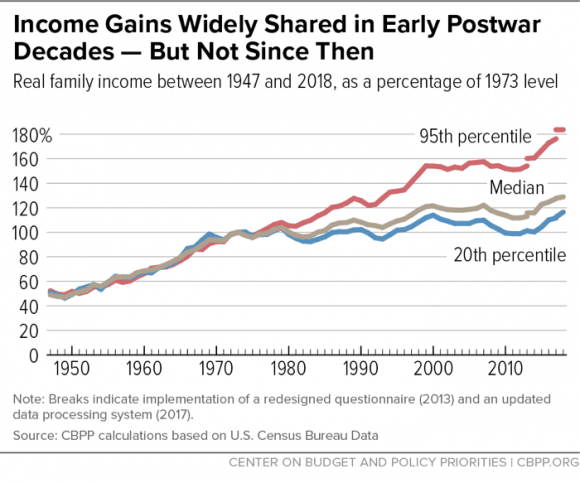

It stands to reason that if wages are not growing since the 1980s then how do you increase your wealth? You need to own things. Homes. Shares. Capital. The more things you own the better. How do you own more with limited cash? Leverage! Low interest rates are great for borrowing. Unfortunately leverage is a double edged sword that is great for those that can use it to scale ownership of assets, not so great for those trying to gain access to assets to keep up. The more assets you have, the more you can borrow, the more you can profit from the gains in capital appreciation. The longer interest rates stay low, the more capital appreciation takes place and the cycle grows.

The rise in financial markets and housing values can only help those most able to play the game. Meanwhile the rest of society is mired in debt. Before Covid the average UK household was experiencing debt levels (excluding mortgages) 50% higher in ten years. If you aren’t able to play the game it is because you are too busy trying to pay off debts to bother entering the stock market.

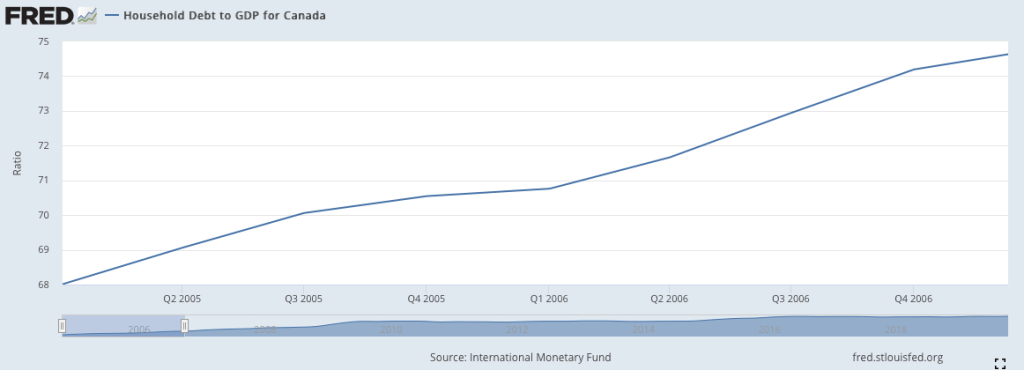

Canada, which was praised for avoiding much of the bloodbath that was the financial crisis has also seen household debt levels rise, while interest rates also declined.

Meanwhile government debt just keeps piling up. Developed economies can’t afford higher interest rates. There is no way to see this changing anytime soon.

Low interest rates contributed in part to the bubble in 2007. We have witnessed this phenomenon several times (see: Japan 1980s). Interest rates are never widely promoted as the main culprit, but they are always near the crime scene. However, cutting interest rates can only go so far and central bank policy in the 21st Century applied all kinds of new techniques to inject money into the financial system. Stock markets are at all time highs despite a massive pandemic that continues to hamper large segments of our economies with limited optimism in sight. What happens when central banks try to reverse this process? Stock markets begin to puke gains. We saw this in late 2018. Yet if you read that linked article from CNBC you will see the same press outlet moved quickly to remove any culpability on the part of the central bank after the fact. If you are a critic of the fed you are likely to be labelled as a “gold bug nut” or a “conspiracy theorist”. Yet the longer this insanity goes on, the more right those critics appear to be.

Why does this continue? Wealth preservation. It appears central bankers do not wish to let the market find a floor at any cost. Who benefits? Baby boomers have worked hard to accumulate all of this wealth and the powers that be in the same age bracket do not want to let go of it while they can still enjoy it. So it will continue until the system breaks and no longer can withhold the tide of wealth destruction. The higher prices rise, the further they have to fall. The lower rates are, the more debt is in the system. For the majority not in the top tier of wealth they will cut vicously from both sides when the tide turns. Their children and generations after are likely to suffer the consequences of this form of greed.

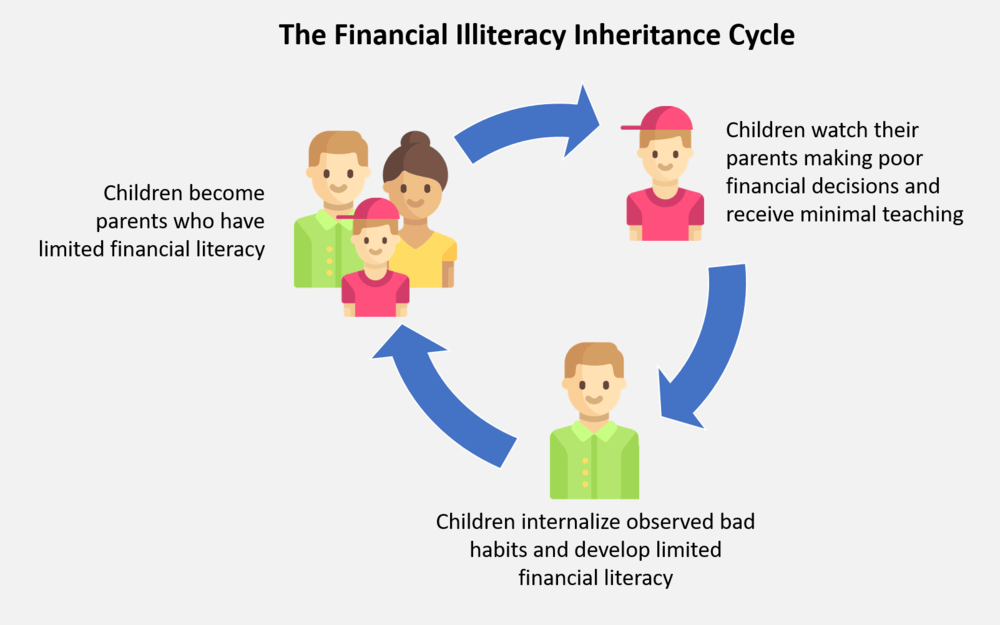

What is worse is that much of this material appears largely misunderstood by the majority of the public. Not the fact that prosperity is weakened, but the role interest rates and central bank intervention have played in creating this situation. There is massive financial illiteracy across our society and it is a cycle that grows and pits more and more at a severe disadvantage in a system already with the odds stacked against them. Instead of focusing on the technical aspects of fed policy and its unintended (or intended) consequences, everyone is being distracted by all types of politicised problems for society’s ills. Austerity, manufacturing job losses, social justice, capitalism itself. This misses the mark by a wide margin and offers no meaningful solutions for inequality, or greed for that matter.

It isn’t just the children of CEOs that are struggling on their own to achieve their parents’ levels of wealth. If you were a middle income boomer you likely accumulated decent wealth through housing and established enough disposable income to raise and educate a family. This is no longer accessible to their children by themselves. It is determined today’s youth need the wealth transfer to experience a lifestyle on par with their parents. The situation is worse for any using debt to try and leave behind as much as possible. The irony is that the older generation de-facto supports central bank policy to their detriment. Or at least that of their children. It is a form of greed acceptance, even if unknowingly. Greed takes the form of an intense and selfish desire to have more of something. In the 21st Century, low interest rates and central bank saviours are the tool to maintain the desire for what has been but that, left to its own devices, can no longer be.