By Bane

This post was written on June 28, 2020.

Volatility Continues

It was a week where the NASDAQ hit an all-time high, Gold hit an 8-year high, a major accountancy scandal brought down a major digital finance firm, markets started the week up big, then turned around and finished the week in the red. It is hard to make sense of it all. The NAS and Gold hit those high levels ON THE SAME DAY. But if you step back and take a look at a long horizon the noise gets quiet and you will notice some steady trends.

Commodity Rally

Gold has been steady and even reached a 5k year high in terms of the gold / silver ratio. Consider the divide between paper and physical pricing and the ratio is likely even higher.

One other point that may be connected. I’m not sure how accurately the price of gold that I see on my screen reflects the actual demand. The gold marketseems split at the moment: while the price is falling, meaning there are more sellers than buyers, everything I read on Twitter is that physical gold is nearly unobtainable – many banks and refiners have run out of inventory. Apparently there has been a surge in retail demand for gold coins and bars at the same time as the price has been falling. It seems that the “paper” market, the futures and ETFs, is determining the price and does not reflect the heightened demand on the street for hard metal during this time of insecurity. In that case, gold prices could be even higher and the ratio even higher than what we see.

One thing to remember is the last time everyone was big into technology stocks oil was forgotten. What occurred after was a massive boom in energy prices that died out in 2015. This isn’t to say that there will be another energy boom as there are lots of problems, notably in shale as highlighted in the bankruptcy of Chesapeake – the godfather of shale drilling. It’s complicated by the fact renewable energy sources are becoming cheaper, so perhaps oil could be the new tobacco. Tobacco stocks were not a bad place to have your money. There could be fewer producers left after all this calamity but they could be set up to benefit from any future bounce back in oil prices.

That said, anyone who went in on oil stocks in 2007 when the market was hot are likely still in the hole as the share prices tend to underperform the commodity itself.

Anyone who experiences this kind of pain, as I am familiar with, is likely to learn from it. Unfortunately there’s an entire new generation of traders and investors that have not had to experience this since Central Banks inflated share prices after 2008.

Time Horizon and Point of Entry Matters

If you bought the FTSE in the late 90s, you would have only recently experienced green territory and if you had not got out before the recent downturn you lost that momentary period of ecstasy. If you were 25 in 1999, you are 46 years old this year and time is getting short. With heavy risks to the downside if you go in now, keep in mind how long it can take to get back to even after any substantial downturn.

Remember that rule when looking at the NASDAQ. It took holders in ’99 over a decade to get back to even.

Debt, Debt and more Debt

Bloomberg chart shows bankruptcies spiking:

We are only starting to see the impact on businesses. A quick recovery is hoped for but given all the complicated rules and signs of localised lockdowns, that recovery looks tepid and volatile at best. The bills won’t stop coming.

Other leverage and default issues are already showing warning signs of areas to be concerned about:

- There is a looming domino crisis in commercial real-estate, as the example of Brookfield demanding rent while skipping its own mortgage payments

- Canada’s debt has been downgraded by Fitch. There is massive consumer and corporate debt in Canada that has been building for such a long time. This does not bode well for Canada. Huge bailouts could be required in the future.

This suggests, if Raoul Pal is correct, we may be heading into the insolvency phase of the crisis.

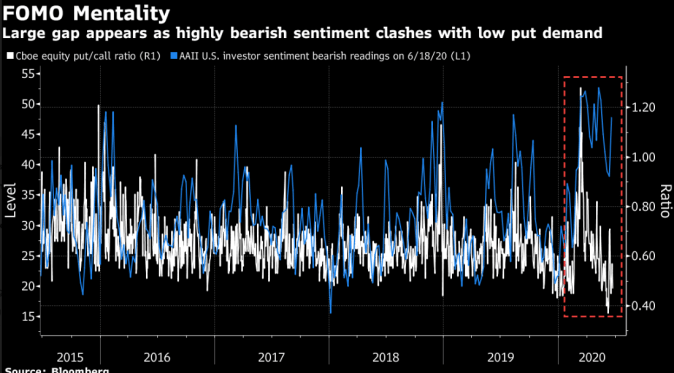

Just Buy

According to a Bloomberg chart, while professional investors remain bearish they aren’t putting their money where their mouth is.

From Bloomberg:

Investors looking for evidence of the fear-of-missing-out mentality prevalent in today’s stock market should keep an eye on the unusual gap that’s opened up between a gauge of sentiment and one of action in U.S. equities. While bearish readings from the American Association of Individual Investors have jumped to a historically high level, demand for downside protection via the options market remain very subdued, according to the Cboe’s ratio of puts to calls. That suggests investors are swallowing their fears and continuing to maximise their exposure to any upside. As Citigroup’s Tobias Levkovich describes it, it’s a case of the concerned investor not putting their money where their mouth is. Still, signs of both bullishness and bearishness were clearly evident in Tuesday’s trading. The Nasdaq 100 closed at a record, yet gold rallied to its highest in eight years.

The pressures on fund managers during this time are immense. They have to perform. Personal or individual investors have the luxury of being able to sit things out. The choice is yours. Given heavy retail buying however, that is not taking place. But maybe there is something more to that.

Portnoy’s People

I’ve had a change of heart. Perhaps the Portnoy period says something more than just retail investors are playing with fire.

“I’m not saying I had a better career. … He’s one of the best ever to do it,” he said. “I’m the new breed. I’m the new generation. There’s nobody who can argue that Warren Buffett is better at the stock market than I am right now. I’m better than he is. That’s a fact,” he said.

Maybe this is a revolution of sorts. That Central Banks have created an essential gambling ring where everyone is playing poker. The greatest bluff of all time. A world where fundamentals no longer matter. If everyone went in investing in the market using a completely new bag of tricks to invest, then all logic goes out the window and the market is completely unpredictable. Perhaps it will take a long period of this insanity to blow things up and force the decision makers to reflect on their ways. Unfortunately, int he long run fundamentals do matter and when they come home to roost it will not be pretty. As much as it will be nice to reflect on how irresponsible these policy decisions have been, we may have more pressing issues to deal with when that happens.